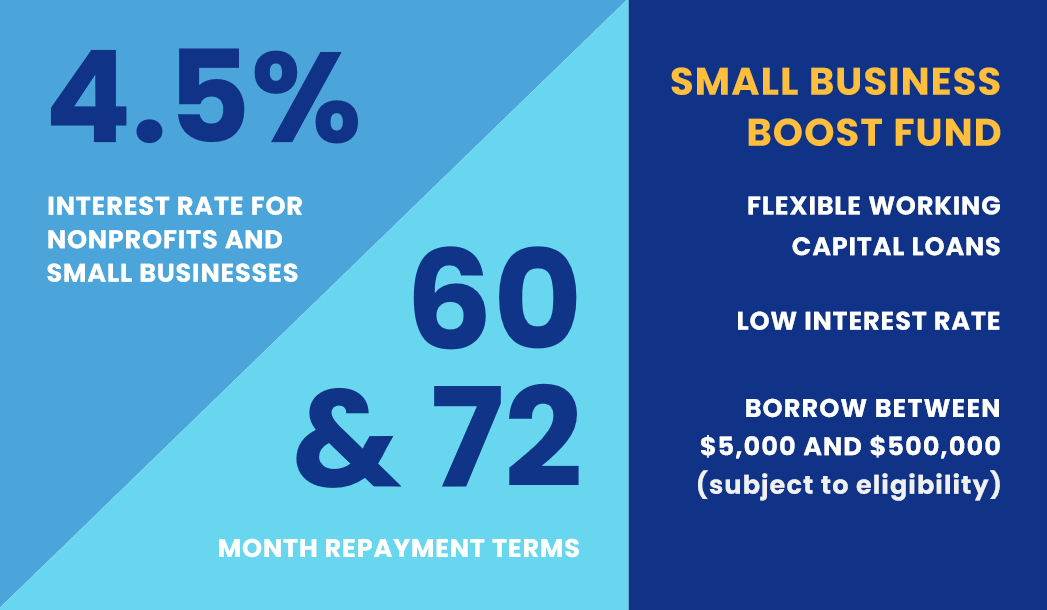

A straightforward, low-interest loan tailored to Connecticut’s small businesses and nonprofits.

THE CONNECTICUT SMALL BUSINESS BOOST FUND is a new resource that will move your business forward.

Supported by the CONNECTICUT DEPARTMENT OF ECONOMIC & COMMUNITY DEVELOPMENT, the Fund links you to the financial support you need to thrive.

Many small businesses and nonprofits in Connecticut experience barriers to accessing financial resources. This is especially true for organizations in distressed municipalities and those led by women, individuals with disabilities, veterans, and people of color.

The Connecticut Small Business Boost Fund was created to provide access to working capital for those who need it most, supporting a greater economic recovery for Connecticut. Expand the tabs below to learn more.

Once you've reviewed the information, be sure to visit CTSMALLBUSINESSBOOSTFUND.ORG to pre-apply.

ELIGIBILITY REQUIREMENTS

ELIGIBILITY REQUIREMENTS

- Must have operations in Connecticut

- No more than 100 full-time employees

- Annual revenues of less than $8 million

- Businesses and nonprofits must have been in operation for at least 1 year prior to the date of application

- A small amount of financing is available for start-ups

Please note: Even if you meet these conditions, you will be disqualified if you have:

- Active bankruptcies

- Unpaid child support

- Outstanding tax liens/judgments

You also must be up-to-date on all your state obligations (local and state taxes, and any prior state lending programs), and you must show you have the ability to repay this loan.

INELIGIBLE APPLICANTS:

Include:

- Corporate-owned franchises

- Payday loan stores

- Adult bookstores, strip clubs, or massage parlors

- Passive real estate investments

- Lobbying firms

- Pyramid sales schemes firms

- Cannabis businesses or firms engaged in activities that are prohibited by federal law or applicable law in the jurisdiction where the business is located

- Gambling

- Speculative business firms such as commodity futures trading or passive real estate investing

- Applicants delinquent on another similar loan

- Loan applicants that are delinquent on state or local taxes

Applicants delinquent on any state obligations